Advanced Relative Strength backtest example

Jan 31, 2012

in Relative Strength

Q. "How do I test a strategy that combines the top relative strength ETFs from 2 or 3 separate portfolios?"

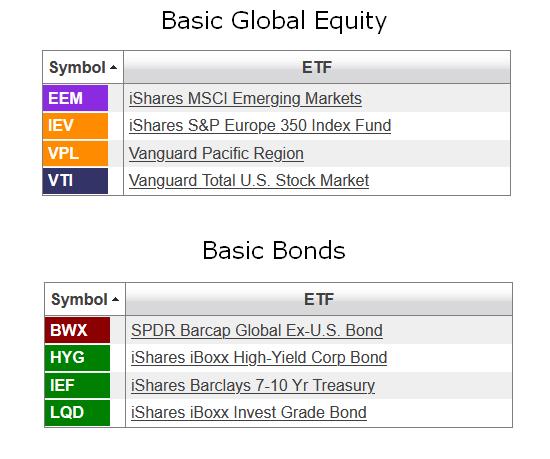

A. Create your chosen portfolios

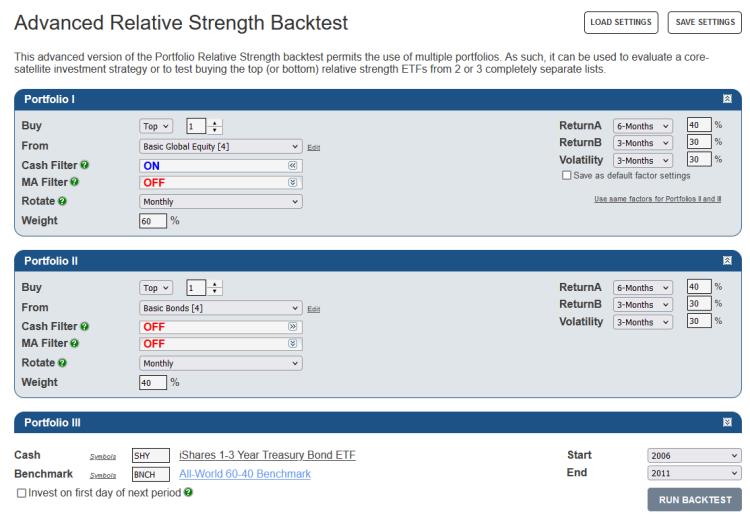

Go to the Advanced Relative Strength Backtest, select your portfolios and choose your settings.

With the 'Cash Filter' ON, the top ETF(s) must be ranked above the cash ETF (SHY), otherwise the backtest will switch to that cash security.

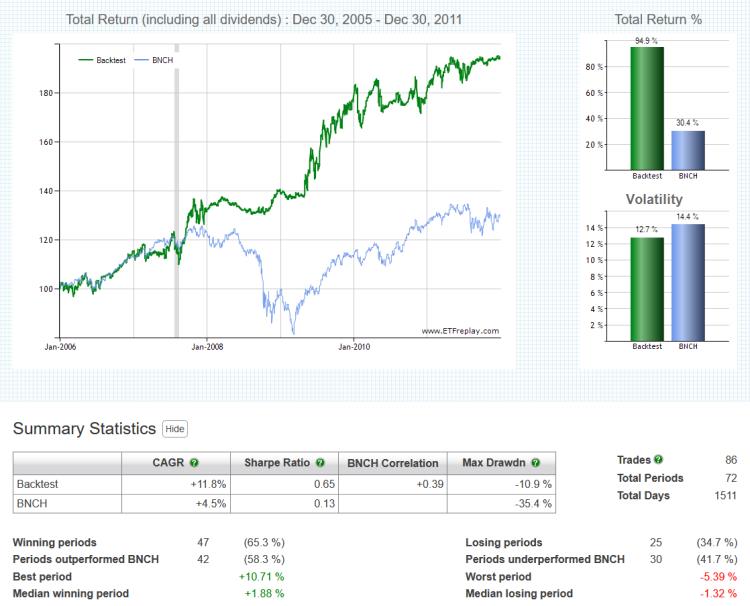

Click 'Run Backtest' and view the charts and summary statistics.

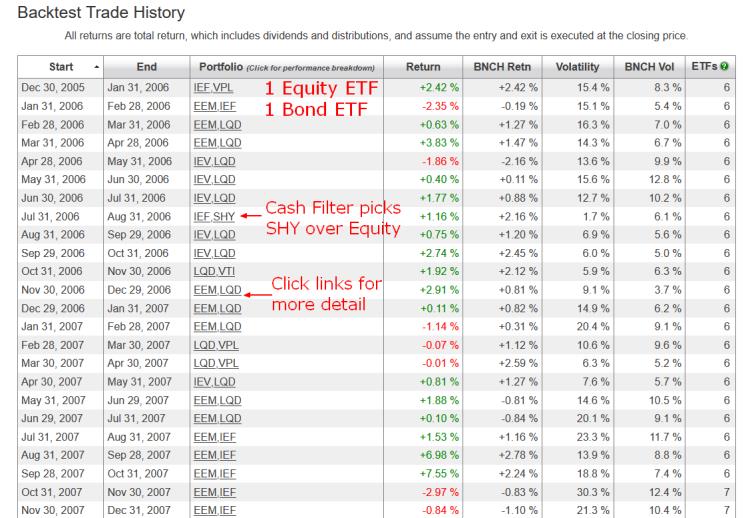

The 'Backtest Trade History' table displays the dates of all trades (entry and exit) and the performance of both the backtest and benchmark.

Click on the ticker symbols in the 'Portfolio' column of the 'Backtest Trade History' table for any period and a pop-up window will appear displaying the starting weight of each security and its return contribution.

Please note that this is purely an illustrative example of one way to use the Advanced Relative Strength backtest and in no way does it constitute investment advice. The portfolios were chosen for information purposes only.

Follow ETFreplay on